In this post we show that an increase in aggregate demand first generates an increase in the use of productive equipment and then an increase in productive capacity. This suggests we do not need to worry about inflation after a fiscal or monetary stimulus to boost aggregate demand, but can rather expect higher investment in the long term along with utilisation returning to its pre-shock levels.

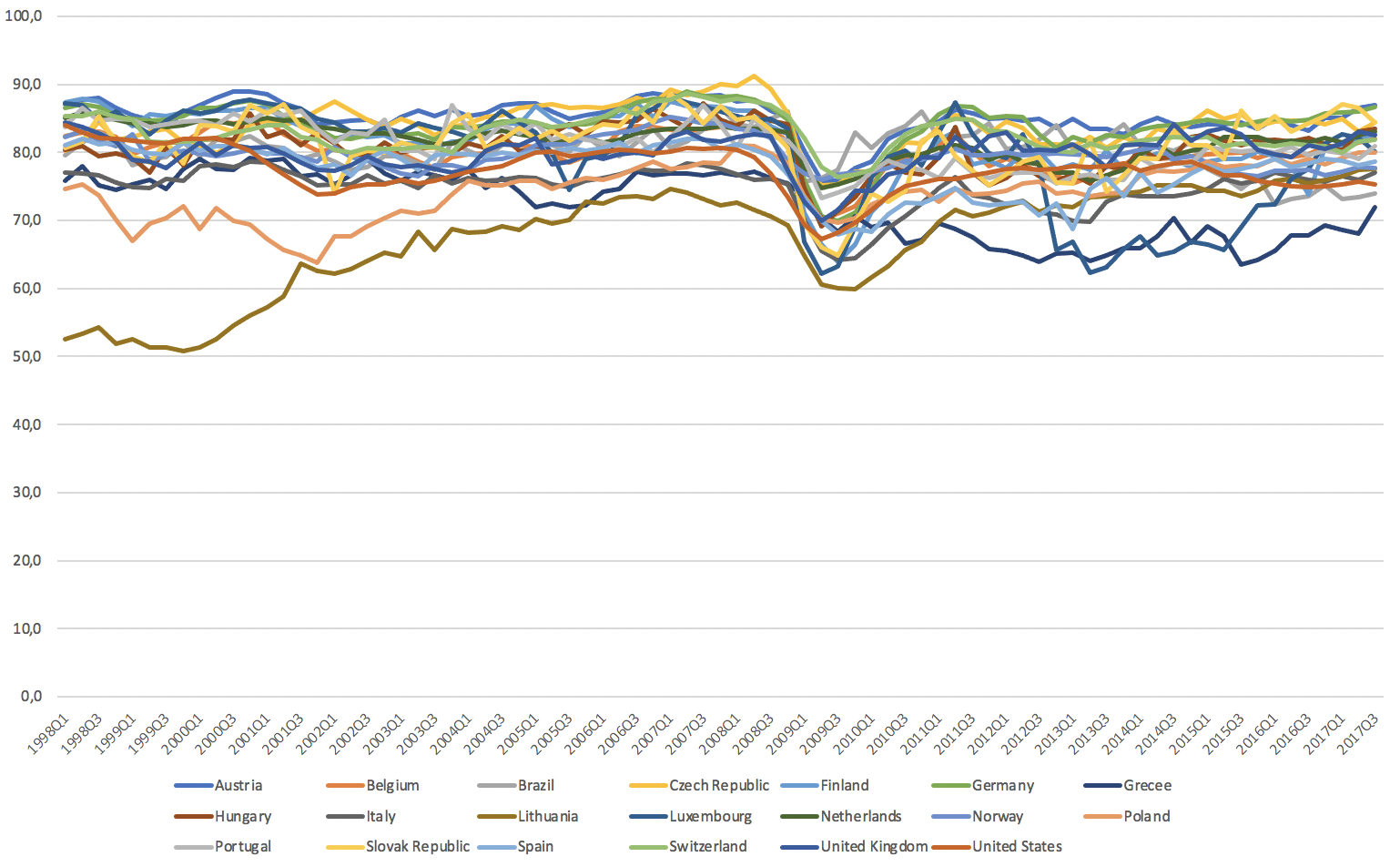

A stylised fact that characterises modern economies is that part of the installed productive capacity is persistently idle. By productive capacity I mean the productive equipment (mostly fixed capital goods) in existence, together with that part of the workforce which is required to operate it. As we can see in Figure 1, in countries as diverse as Belgium, Finland or Lithuania, the effective utilisation of installed capacity often gravitates below 100%, and around 80% on average worldwide.

Figure 1. Installed capacity utilisation by country (1998Q1-2017Q4).

Source: see Appendix I.

The academic consensus is that there are large margins of idle capacity planned by entrepreneurs. The reasons why entrepreneurs plan to operate with idle capacity vary according to the school of thought considered. At the risk of making a drastic simplification, we can say that while some authors think that entrepreneurs do so in order not to lose market share in the face of changes in demand, others tend to think that there is a rate of utilisation of installed capacity that does not accelerate inflation (Non-accelerating inflation rate of capacity utilisation, NAICU).

Read more of this post

No comments:

Post a Comment